July 9, 2026

Finding Your SOC, Audit, and Tax Competitive Edge

You just landed your third carrier partnership this year. Your platform is handling real volume. Then a client’s vendor management team drops a checklist on your desk: SOC 2 report, audited financials, state tax documentation. The product is ready. The back office isn’t.

One firm for the SOC report. Your board wants a different firm for the financial statement audit. Your existing tax advisor still doesn’t understand your revenue model. Three firms. Three invoices. Three sets of calls pulling your team away from product development.

Growth is working against you, not because the business is struggling, but because the back office hasn’t kept up. For small and midsize insurance-adjacent tech companies, this is one of the most avoidable scaling mistakes.

The Moment You Outgrow QuickBooks, and Your Vendor Stack

Early on, everything is manageable. QuickBooks handles the accounting. A local firm files the tax returns. Nobody asks about your control environment because you’re small enough to fly under the radar.

Then the business matures. A carrier client asks for a SOC 2 Type II before renewing. Your state tax footprint spans eight jurisdictions because you hired remote employees. The board wants audited financials. Your entity structure, fine when you were five people, suddenly needs attention.

Most founders hire a specialist for each problem. One firm for SOC. Another for audit. Keep the existing tax advisor. Logical instinct. Compounding operational mistake.

Why a Generic SOC Firm Is the Wrong Call

Here’s what most growing platforms miss: not all SOC practices are built the same. A generalist SOC firm will assess your controls against standard criteria and hand you a report. But if your platform sells into the insurance ecosystem, standard criteria aren’t what your clients actually care about.

Carriers and MGAs evaluate vendors through a specific lens: data handling practices, claims processing integrity, regulatory expectations that vary by state and line of business. A firm that doesn’t understand that lens produces a report that checks boxes without addressing what your clients are really looking for when they review it.

Johnson Lambert has spent more than 40 years inside the insurance ecosystem, serving more than 750 insurance-related organizations nationwide. That means the team already knows what your carrier clients expect to see in a SOC report, because they’ve spent decades working on the other side of that vendor checklist. The controls framework Johnson Lambert builds with you isn’t generic. It’s shaped by direct knowledge of how insurance companies actually evaluate the platforms they partner with.

Our specialization turns your SOC report from a compliance checkbox into a business development asset. When a prospective carrier client reads it, they see a control environment that speaks their language — not a boilerplate document they have to interpret.

A SOC Practice Built Around How Insurance Tech Companies Actually Scale

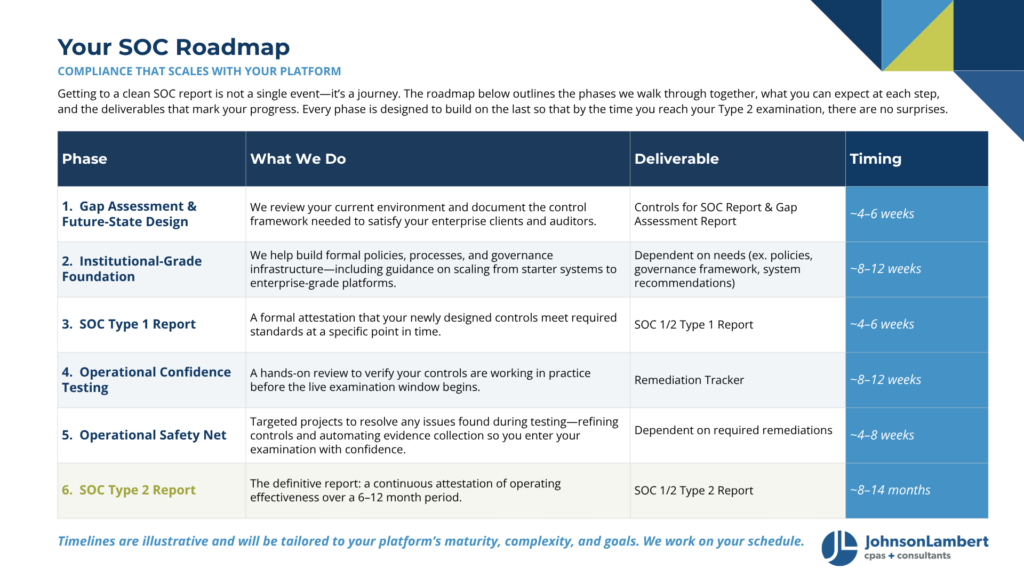

Johnson Lambert’s SOC practice isn’t a single engagement, it’s a roadmap designed around the way insurance-adjacent platforms grow, from early-stage controls through mature, automated compliance operations.

Starting with infrastructure. When platforms migrate off systems like QuickBooks and onto more robust financial systems, Johnson Lambert guides the transition so new infrastructure is audit-ready and SOC-compatible from day one — no retrofitting controls after the fact.

As the platform matures, the focus shifts to efficiency. SOC audits consume developer time, pulling screenshots, compiling access logs, documenting change tickets. Johnson Lambert builds toward automating evidence collection, freeing your team to build product instead of assembling compliance binders.

The roadmap is designed so each stage feeds the next, building compliance infrastructure that compounds in value rather than resetting every audit cycle.

SOC, Audit, and Tax — Coordinated

The operational payoff of Johnson Lambert’s insurance specialization extends beyond SOC. Financial statement audits and SOC examinations share significant underlying control work, logical access security, change management protocols, IT governance. When the same firm evaluates both, overlapping controls are tested once and mapped to satisfy multiple requirements.

Test once. Satisfy both. That saves weeks of redundant fieldwork, time, and budget that matters far more at a 30-person company than a Fortune 500.

Johnson Lambert layers three capabilities into a coordinated engagement:

- SOC Readiness & Reporting — Type I and Type II examinations shaped by decades of insurance industry experience, built for platforms whose clients expect that level of specificity.

- Audit & Assurance — GAAP-compliant audited financial statements that satisfy your board, your banking relationships, and your carrier partners. Coordinated alongside the SOC engagement so your team handles one information request, not two separate fire drills.

- Tax Advisory — Entity structuring, multi-state compliance, and revenue stream analysis for platforms whose tax footprint is expanding faster than their headcount. Your tax posture stays aligned with your audit and SOC scope, not siloed from it.

Start Building with a Firm That Knows Your Market.

If your compliance vendors don’t understand the insurance ecosystem you sell into, you’re not just wasting coordination time, you’re leaving value on the table every time a carrier client reviews your SOC report.

Talk to Johnson Lambert about a SOC, Audit, and Tax roadmap built specifically for insurance tech, one that turns compliance from an operational headache into a reason carriers want to do business with you.