April 25, 2017

Master Trust Reporting Changes Are In

In December we shared information regarding Proposed Changes to Master Trust Reporting and the implications to employee benefit plans (EBP) that invest in master trusts. The proposal was adopted and the final ASU 2017-06, Employee Benefit Plan Master Trust Reporting has been released.

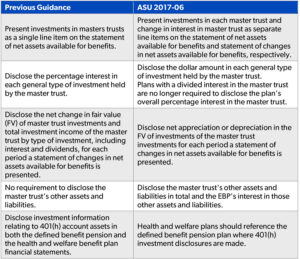

The following highlights some of the changes from the previous guidance versus the new ASU:

This ASU is effective for fiscal years beginning after December 15, 2018 with early adoption permitted. The amendments should be applied retrospectively and EBPs should disclose the nature and reason for the change in accounting principle in the year of adoption.