December 12, 2023

Navigating the Corporate Transparency Act: Beneficial Ownership Information Reporting

The Corporate Transparency Act (“CTA”) created the beneficial ownership information (BOI) reporting rule, scheduled to take effect on January 1, 2024. The CTA is poised to usher in significant reporting requirements for both domestic and foreign entities operating in the United States. In this article, we will delve into key components of the BOI reporting rule, reporting obligations, and ongoing developments related to the Act.

Purpose of the CTA: Unveiling Transparency Against Illicit Financial Activities

The CTA emerges as a robust response to combat the misuse of shell corporations and entities in facilitating money laundering and illicit activities. At its core, the CTA mandates that “Reporting Companies” provide specific information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN), an agency under the U.S. Department of the Treasury. The CTA authorizes FinCEN to collect, protect, and disclose this information to authorized governmental authorities and to financial institutions in certain circumstances.

Our firm is sending you this communication to provide you with some general information regarding the new reporting rules as well as initial steps you should take to address the implications of the CTA to your organization.

Applicability of Reporting Requirements: Who Needs to File

The scope of the CTA extends to both domestic and foreign entities that undergo registration with a secretary of state or an equivalent office. This includes various business structures such as corporations, LLPs, and LLCs. Entities failing to meet exemption criteria are obligated to adhere to the reporting rules outlined by the CTA.

Good news is there are 23 exemption categories. While not all inclusive, ones that might be most applicable are:

- Insurance Companies

- Inactive Entities

- Not-for-profit Entities

- Pooled Investment Vehicles

- Subsidiaries of certain exempt entities

- Large Operating Corporations

As noted above, a large operating corporation will likely be one of the most applied exemptions. A large operating corporation, as defined by the CTA, must have a U.S. physical office where it conducts its business operations, more than 20 full-time employees in the U.S., and has filed federal income tax returns that show total gross receipts or sales of more than $5,000,000 (earnings may include the main entity and other entities it owns and operates through).

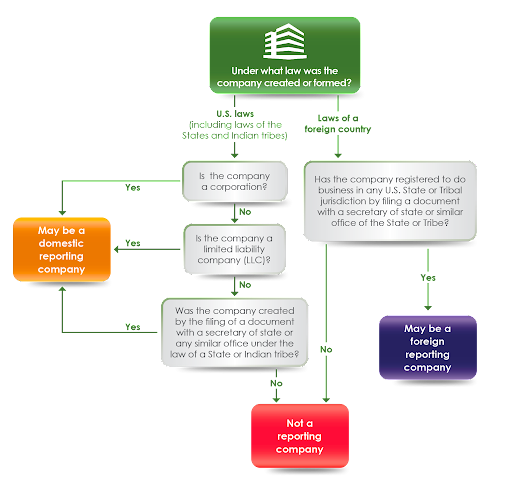

When assessing the requirement to file this report, it is recommended to seek guidance from your legal advisor for a comprehensive evaluation. The flowchart below illustrates which entities will possibly be subject to reporting.

FinCEN’s Small Entity Compliance Guide Reporting Company Flowchart1

Identifying Beneficial Owners: Decoding Substantial Control and Ownership Interests2

Beneficial owners are defined as individuals with at least 25% ownership interests or those who directly or indirectly exercise substantial control over reporting companies. Substantial control can be established through senior officer roles, authority over appointments or removals of senior officers or majority of the board, or has substantial influence over pivotal decision-making. Therefore, senior officers and other individuals with control over the company are beneficial owners under the CTA, even if they have no equity interest in the company.

In addition, individuals may exercise control directly or indirectly, through board representation, ownership, rights associated with financing arrangements, or control over intermediary entities that separately or collectively exercise substantial control.

Information to be Reported: What to Report

Reporting companies are responsible for furnishing the details about themselves and their beneficial owners.

The required information will include:

- Full legal names

- Jurisdiction of formation

- Dates of births

- Addresses (personal addresses for the beneficial owners)

- Identification documents (EIN, drivers license, passport, etc)

Reporting Companies will need to rely on beneficial owners to timely update any reportable changes to their information (e.g., ownership changes, moves, marriages, divorces, etc.). As a result, a company’s operating documents may need to be revised to include provisions related to the CTA such as representations, covenants, indemnifications, and consent clauses.

Information Deadlines: When to Report

For reporting entities established prior to January 1, 2024, the deadline for submitting their initial BOI reports to FinCEN is extended until January 1, 2025. Reporting entities formed in 2024 have 30 days (Proposed extension to 90 days for 2024) to report the required information.

FINCEN has also established a 30-day period for any modifications to the BOI report. These modifications encompass changes such as name alterations, any new individuals who meet the threshold criteria, instances of mortality, changes in C-suite officers, or the transition of a beneficial owner from a minor to adulthood. Timely communication of such changes is crucial to guarantee adherence to reporting obligations.

Currently, we are awaiting additional guidance from FinCEN and states in regards to our ability to provide assistance on the CTA filings. As the CTA is not a part of the tax code, the assessment and application of the regulations may necessitate the need for legal guidance. As such, our firm is still accessing what role we can play.

Note that penalties for willfully violating the CTA’s reporting requirements include (1) civil penalties of up to $500 per day that a violation is not remedied, (2) a criminal fine of up to $10,000, and/or (3) imprisonment of up to two years.For additional information regarding the beneficial ownership reporting requirements under the CTA, refer to FinCEN’s Frequently Asked Questions document.

Morgan Potter

Tax Senior Manager