October 16, 2020

Nonprofit ASU 2020-07 News: Contributed Nonfinancial Assets

As expected, the Financial Accounting Standards Board (FASB) issued Accounting Standard Update (ASU) 2020-07, Not-for-Profit Entities (Topic 958): Presentation and Disclosures by Not-for-Profit Entities for Contributed Nonfinancial Assets, which addresses presentation and disclosure requirements for contributed nonfinancial assets commonly referred to as gifts-in-kind.

The ASU requires nonfinancial contributed assets, the use of nonfinancial contributed assets, or contributed services meeting the criteria for recording be presented separately from contributions of cash and other financial assets in the statement of activities. Additionally, disclosure of the programs or activities for which contributed services were used is required. Examples of nonfinancial contributed assets include land, building, and equipment; supplies and materials, such as food, clothing or pharmaceuticals; and intangible assets.

Nonprofit organizations are required to disclose the following:

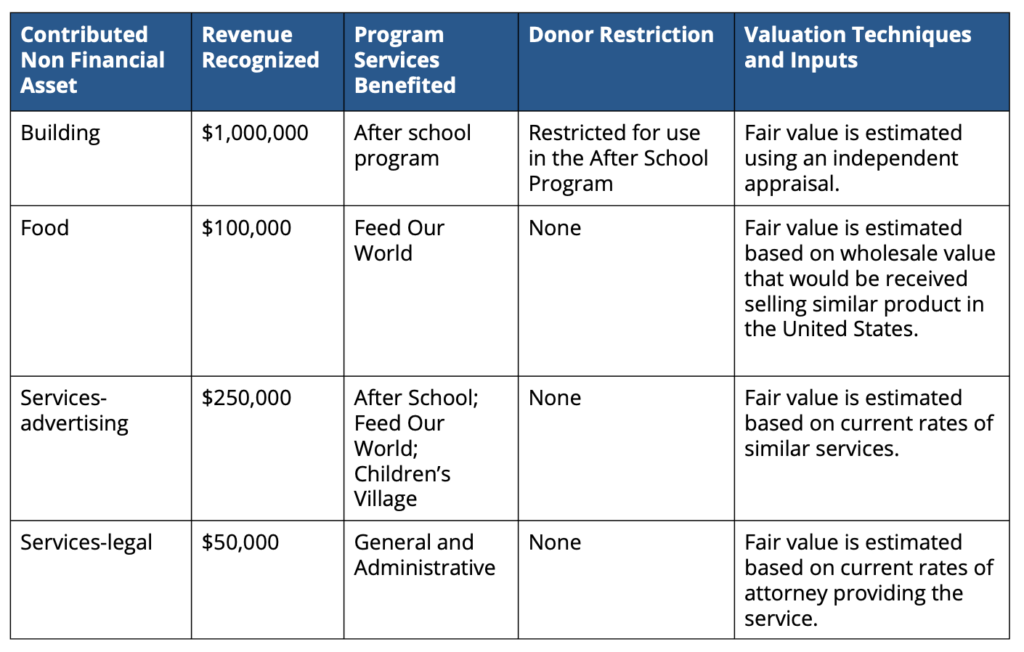

- Contributed nonfinancial assets disaggregated by category;

- Qualitative information, by disaggregated category, about whether the contributed nonfinancial assets were or are intended to be either monetized or utilized during the reporting period and future periods. If utilized, a description of the programs or other activities in which those assets were or are intended to be used;

- The existence of donor restrictions, by disaggregated category; and

- The valuation techniques and inputs used to arrive at a fair value measure, by disaggregated category, in accordance with the requirements of the Fair Value Measurement guidance found in ASC Topic 820.

- The principal market (or most advantageous market) used to estimate fair value if it is a market in which the nonprofit is prohibited by donor restriction from selling or using the contributed nonfinancial asset.

The ASU addresses presentation and disclosure and does not provide guidance on the valuation of contributed nonfinancial assets. The ASU provides several examples of what disclosures related to contributed nonfinancial assets could look like. The following is one example:

ASU 2020-07 is effective for annual periods beginning after June 15, 2021 and should be applied on a retrospective basis. Early adoption is permitted. To obtain information about this and other ASUs and accounting standards visit Fasb.org.

If you have any questions about this, contact the Johnson Lambert team.